Brazil is the clearest proof that instant, account-to-account payments can scale. Pix, the public digital rail operated by the Central Bank of Brazil (BCB), moves money in seconds, 24/7, and works across banks, wallets, and government entities. Its design—neutral infrastructure, open participation, and QR-first user journeys—has turned “paying with Pix” into a default behavior rather than a niche alternative. Central Bank of Brazil

Pix’s scale is not theoretical. The network has logged single-day volumes above 275 million transfers, and soon after surpassed 290 million—numbers you typically associate with peak shopping seasons, not just P2P moments. These records reflect how Pix now underpins merchant payments (P2B) 与 platform payouts (B2P) as much as everyday person-to-person transfers. Agência Brasil

Why Pix keeps winning

It’s instant and interoperable by design.

Pix is public infrastructure with standardized QR codes (static and dynamic), bank-app deep links, and always-on settlement. Because the BCB acts as a neutral facilitator, private players—banks, acquirers, PSPs, and gateways—compete on experience, reliability, and value-added services rather than on access. Central Bank of Brazil

It’s expanding beyond single payments.

The central bank introduced Pix Automático, a native way to authorize recurring charges (utilities, streaming, SaaS, gyms) without card rails or clunky debit mandates. Analysts expect this feature alone to channel tens of billions of dollars in online purchases once fully ramped. The bank also announced Pix Parcelado, which brings Brazil’s beloved installment culture to instant payments: consumers pay over time, while merchants receive funds upfront. Together, these features push Pix deeper into retail and subscriptions—use cases historically dominated by cards. Reuters

It invests in safety nets.

The BCB has strengthened MED (Mecanismo Especial de Devolução)—Pix’s special return mechanism—by updating the rulebook and clarifying evidence, timelines, and device/limit controls. For merchants, MED-aware flows reduce support overhead and build trust without adding friction to checkout. Central Bank of Brazil

It has a credible cross-border path. Brazil participates in the BIS Project Nexus, a blueprint for linking domestic instant-payment systems so a cross-border transfer can clear in roughly a minute. While not a retail feature you can enable today, Nexus signals a future in which Pix-to-abroad becomes far simpler. BIS

It’s winning the e-commerce mindshare battle.

Independent studies have projected Pix to overtake credit cards in Brazilian digital commerce, a trend merchants already see in checkout analytics as QR and deep-link flows compress abandonment. You don’t have to advertise “alternative payments” anymore; for many Brazilian shoppers, Pix 是 the main way to pay.

Checkout patterns that convert

A Pix-first checkout does not need to be complicated. On desktop, render a dynamic 二维码 with a visible expiry; on mobile, offer bank-app deep links and a copy-and-paste code as a resilient fallback. On confirmation, fire real-time webhooks to release inventory or content instantly and show clear Portuguese status text (“Pagamento confirmado via Pix”). If something goes wrong, present a one-tap retry and structured guidance for erro no Pix (e.g., expired code, app mismatch, or security limits). These are small choices that compound into higher success rates and fewer tickets.

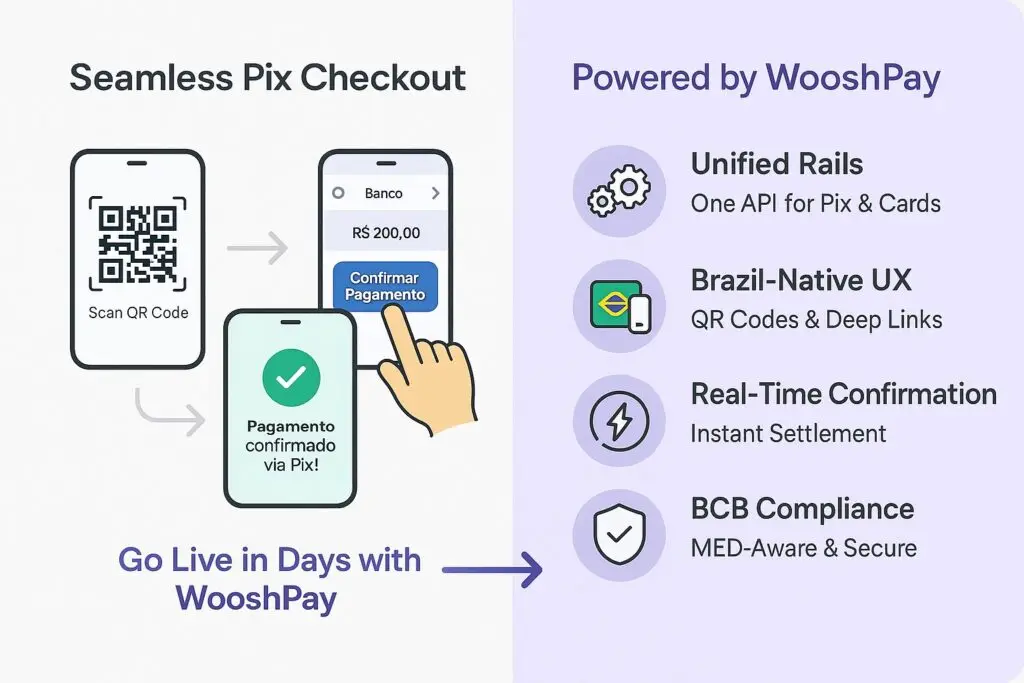

Where Wooshpay helps you win

Unified rails, one integration.

Wooshpay activates Pix and cards (Visa, Mastercard, Amex) through a single API and a single reporting model. You can accept Pix in your e-commerce flow, route intelligently across local rails and acquirers, and fall back to cards gracefully if a QR expires—without stitching multiple vendors.

Brazil-grade UX out of the box.

We ship Portuguese-first checkout copy and help texts, dynamic and static QR generation, copy-and-paste codes, and deep links that open the user’s banking app directly. The goal is a flow that feels native to Brazilian buyers from day one—no plugin patchwork required.

实时 operations and finance.

Webhooks confirm Pix payments in seconds, so orders move immediately and support sees fewer “did my payment go through?” contacts. Our payloads include the Pix transaction data your finance team needs for automatic reconciliation and clean audit trails.

Security that matches the rulebook.

Wooshpay bakes MED-aware processes into refunds and investigations and tracks BCB security updates—like device registration and value limits—so your flows remain compliant by design rather than by periodic cleanups. Central Bank of Brazil

Cash-flow efficiency for everyday baskets.

For catalogs with modest average order values, Pix’s instant confirmation reduces working-capital drag and avoids card-specific overhead. Pairing BRL collection with USD 定居点 (and other currencies as needed) also trims FX leakage and banking complexity for cross-border teams.

Subscriptions and installments without card dependency.

由于 Pix Automático 与 Pix Parcelado gain adoption, Wooshpay exposes them behind simple capability flags in your billing logic, so you can run recurring 与 pay-over-time experiences for buyers who don’t use credit cards—without rebuilding your stack.